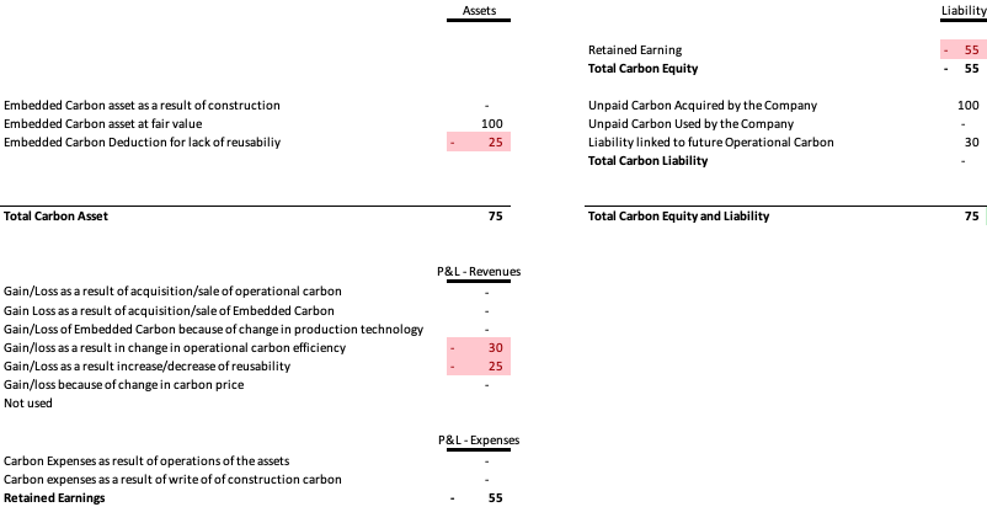

Reporting entity A acquires an existing asset with an Embedded Carbon Asset at fair value of 100 CU. The reporting entity further determine that 25% of the asset cannot be further reused in a future production process. Finally, the reporting entity estimate that the total value of the carbon that will be emitted over the useful life of the asset is 30 CU

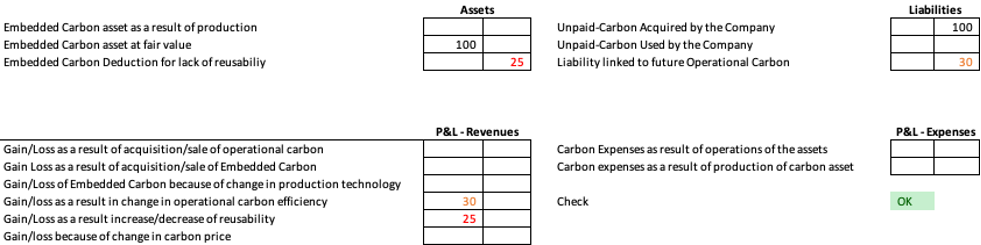

The following bookings would take place:

Theses bookings would lead to the following final Carbon Balance sheet and Carbon Profit and Loss: